-

Ecosystems at the bank account

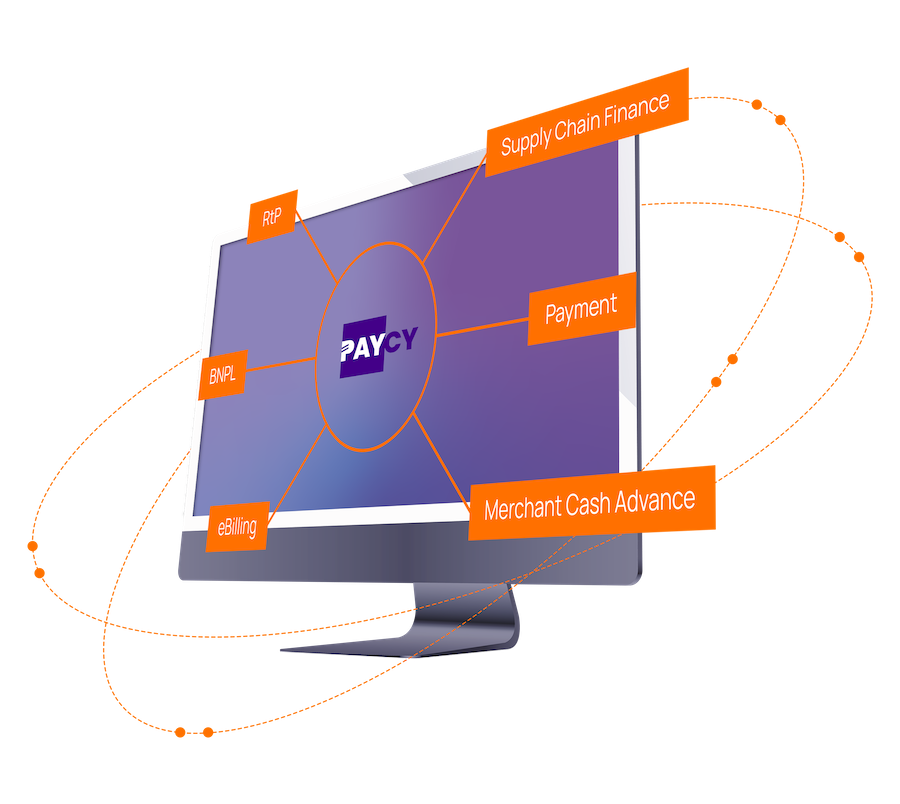

PAYCY for financial institutions

Added value

Offer your customers additional services when paying via PAYCY with Request to Pay.

Customer loyalty

Strengthen the customer-bank interface with PAYCY and interact directly with your customers.

Account

Return the account to its role as the home of money for your customers and corporate clients with PAYCY.

Liquidity

Provide your customers with urgently needed liquidity at the right moment thanks to PAYCY.

Neutrality

Rely on a bank-neutral platform to send and receive Request to Pay transactions.

Independence

Don't make yourself dependent on competitors – rely on PAYCY as an independent platform.